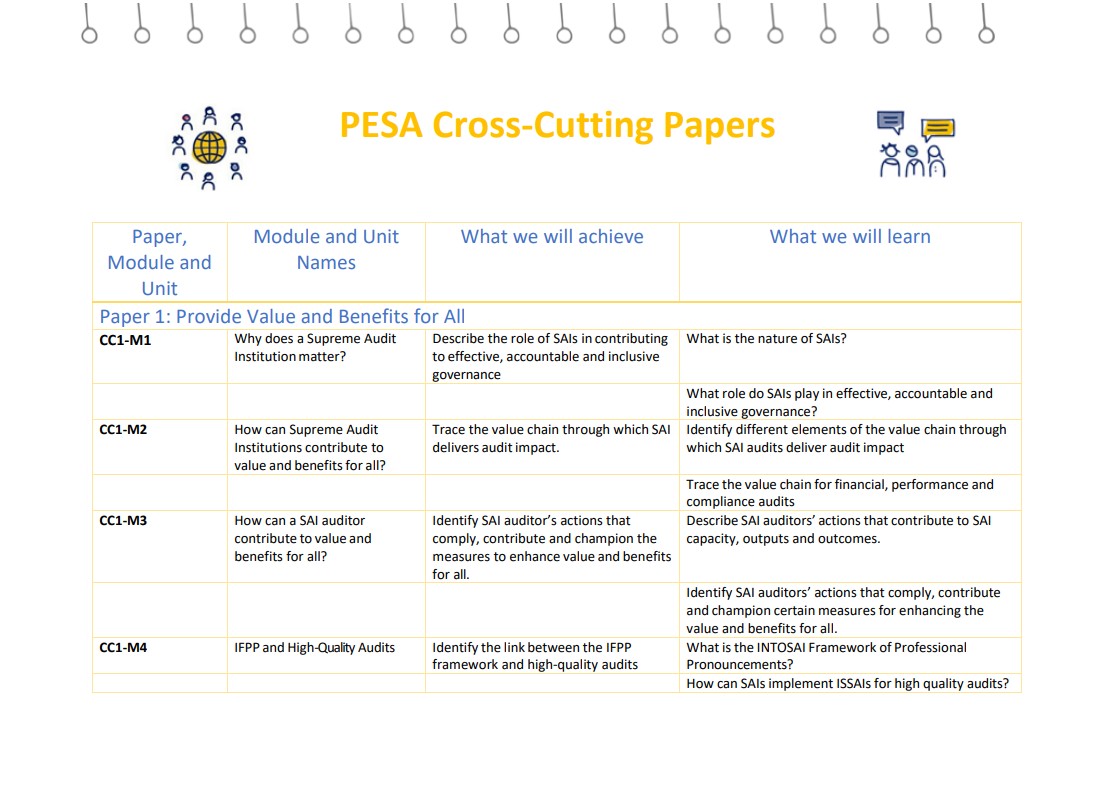

PESA – A Professional Qualification for SAI Auditors

Financial Audit Learning Outcomes

Financial audit learning outcomes start with reflections on the value and benefits of financial audit. Through the five papers, the SAI Auditor is expected to develop knowledge and skills related to, the principles of financial audit and the process of conducting a high quality financial audit as per ISSAIs.

──Financial Audit Mentor

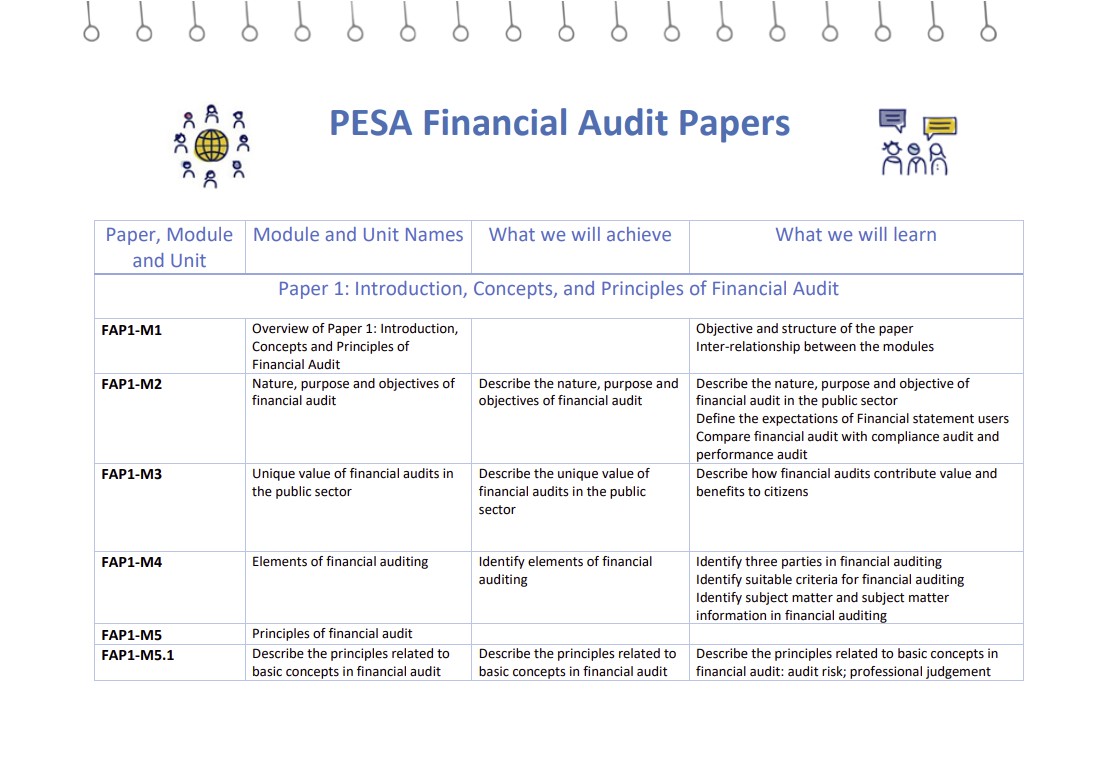

PAPER 1: Introduction, concepts, and principles of financial audit

By studying this paper, the SAI Auditor will achieve the following learning outcomes:

- Describe the nature, purpose and objectives of financial audit in the public sector context.

- Describe how financial audits contribute value and benefits to citizens.

- Identify elements of financial auditing such as three parties, suitable criteria, subject matter and subject matter information in financial auditing.

- Describe the principles related to basic concepts and audit process in financial auditing in the public sector environment.

- Determine with whom to communicate in an entity, explain the matters that need to be communicated, and outline the communication process to be followed in an audit.

PAPER 2: Pre-engagement

By studying this paper, the SAI Auditor will achieve the following learning outcomes:

- Describe the pre-engagement activities for financial audit carried out by SAIs.

- Determine whether the Financial Reporting Framework used for preparation of financial statements is acceptable and assess management’s understanding of its responsibilities in an audit of financial statements

- Select an audit engagement team having appropriate competencies for the given audit engagement

- Describe the ethical declaration required for auditors at the pre-engagement phase of an audit and assess ethical threats and suggest safeguards for the given audit engagement

- Create an audit engagement letter for a financial audit

PAPER 3: Planning and risk assessment

By studying this paper, the SAI Auditor will achieve the following learning outcomes:

- Describe the planning and risk assessment activities and process.

- Describe the process of understanding the entity and its environment including its internal control system and perform analytical procedures in planning the audit.

- Determine materiality and performance materiality for financial statement as a whole and for classes of transactions, account balances or disclosures

- Identify procedures for assessing the risk of material misstatements, identify the financial statement assertions and their role in the audit process, and identify and assess the risks of material misstatements at the financial statement level and the assertions level

- Identify control activities that are relevant to risks of material misstatements and evaluate design and implementation of those control activities.

- Identify responses to assessed risks of material misstatements at the financial statement level and design responses to assessed risks of material misstatements at the assertion level (tests of controls and substantive audit procedures).

PAPER 4: Conduct a financial audit

By studying this paper, the SAI Auditor will achieve the following learning outcomes:

- Describe the pre-engagement activities for financial audit carried out by SAIs.

- Determine whether the Financial Reporting Framework used for preparation of financial statements is acceptable and assess management’s understanding of its responsibilities in an audit of financial statements

- Select an audit engagement team having appropriate competencies for the given audit engagement

- Describe the ethical declaration required for auditors at the pre-engagement phase of an audit and assess ethical threats and suggest safeguards for the given audit engagement

- Create an audit engagement letter for a financial audit

PAPER 5: Completion, reporting and follow-up in financial audit

By studying this paper, the SAI Auditor will achieve the following learning outcomes:

- Outline the process of completion, reporting and follow up phases of the financial audit.

- Evaluate the effect of uncorrected misstatements in the financial statements and their impact on auditor’s opinion.

- Perform overall review of audit engagement to ensure the quality of audit.

- Outline the audit reporting process, describe basic elements of auditor’s report, define different types of audit opinion, compare modification to auditor’s report, and formulate key audit matters, emphasis of matter and other matter paragraphs in auditor’s report.

- Create an audit file by assembling audit working papers and other supporting documents.

- Outline the timing and process of following up on previous and past audit reports.

Available in other languages

DOWNLOAD IN ARABIC

CROSS-CUTTING COURSE OUTLINE IN ARABIC

DOWNLOAD IN SPANISH

CROSS-CUTTING COURSE OUTLINE IN SPANISH

DOWNLOAD IN ARABIC

FINANCIAL AUDIT COURSE OUTLINE IN ARABIC

DOWNLOAD IN SPANISH

FINANCIAL AUDIT COURSE OUTLINE IN SPANISH