by Camilla Fredriksen, Manager, IDI Global Foundations Unit

![]()

In September 2021, the INTOSAI Development Initiative (IDI) released the Global Supreme Audit Institution (SAI) Stocktaking Report 2020, the fourth triennial analysis of data from an INTOSAI Global Survey on SAI performance and capacities. The report, which covers the period of 2017 to 2019, marks the 10-year anniversary of the

Global Stocktaking, which has been an important source of information for INTOSAI and donors about the needs of SAIs.

Many SAIs operate in difficult environments, where mechanisms for accountability are under pressure. Despite these challenges, this year’s Global Stocktaking, which 178 SAIs participated in, paints a picture of an SAI community in which performance and capacities are slowly improving. This article summarizes some of the main messages of the report.

ISSAI-Compliant Practices Require Resources and Robust Quality Systems

Against a backdrop of democratic backsliding and increased levels of corruption, SAIs are making strides to adopt International Standards of SAIs (ISSAIs). These efforts appear to be leading to an improved understanding of what implementation of ISSAIs really entails, including what SAI independence should mean in practice.

ISSAI adoption has increased since 2017, with 86 percent of SAIs reporting they have implemented ISSAIs for their main audit streams. Nearly half of respondents have adopted the standards directly, while the other half have adopted national standards that are based on or consistent with ISSAIs.

More research is needed to fully understand the context of these responses. SAIs that adopt ISSAIs directly may do so because their countries do not have national audit standards.

For the other half, the extent to which national standards are consistent with all elements of the ISSAIs likely varies.

However, the adoption of standards is only the first step, and the Global Stocktaking indicates that for many SAIs, ISSAI- compliant audit practices are still a long way off. While 68 percent of SAIs reported they largely complied with ISSAIs, an analysis of a sample of 42 SAI Performance Measurement Framework (PMF) assessments suggests that this only extended to the quality of audit manuals, and not to audit practices.

In the Global Survey, 44 percent of SAIs said their main reason for not complying with ISSAIs was a lack of resources and limited capacities. Another factor was the lack of a proper quality management system to guide audit processes and address weaknesses in quality systematically. One- quarter of SAIs did not have in place any of the features that comprise a robust quality management system. Considering these challenges, it is encouraging that almost all SAIs were planning to build their capacity in key areas, such as audit planning, implementation, and reporting.

Threats to SAI Independence Remain a Challenge

The report shows clearly that threats to SAI independence remain a serious challenge, with a drop in results for seven of the eight principles of the Mexico Declaration. Unwelcome external interventions limited the ability of SAIs to deliver their mandates, posing serious risks to transparency and accountability. Nearly half of SAIs expressed interest in strengthening their legal framework and independence.

As previous Global Surveys have found, financial and operational autonomy were still the most challenging aspects of independence. Forty percent of SAIs reported they had experienced major interference in budget execution. While SAIs mostly reported a certain degree of autonomy in daily operations, only 63 percent fully controlled staff recruitment, and around 70 percent said their staff was inadequate in either numbers or competence.

SAIs also experienced direct interference from the executive in their audit operations. The most surprising finding was that only 44 percent of SAIs had full, timely access to information for their audits, a 26-percent drop from 2017.

Data also suggests that the selection of audit programs—an area in which most SAIs experienced more freedom—is linked to levels of democracy. SAIs in countries with less democratic space experienced more interference when deciding on their annual audit programs. Reporting on findings was also a challenge, with 12 percent not publishing any reports at all.

Greater Transparency and More Strategic Communication Are Needed

While strengthening SAI independence is critical for the oversight of public spending, the report suggests other important steps SAIs can take to promote transparency and accountability and to enhance their impact.

The report shows that SAIs could be more transparent regarding their own operations. While almost all SAIs had strategic plans, only 57 percent publicly reported the extent to which they met their objectives. Of the 72 percent of SAIs that produced financial statements, only 73 percent submitted them to an external audit, and fewer reported publicly on audit results. Similarly, while many SAIs had conducted SAI PMF assessments, very few had shared their strengths and challenges publicly.

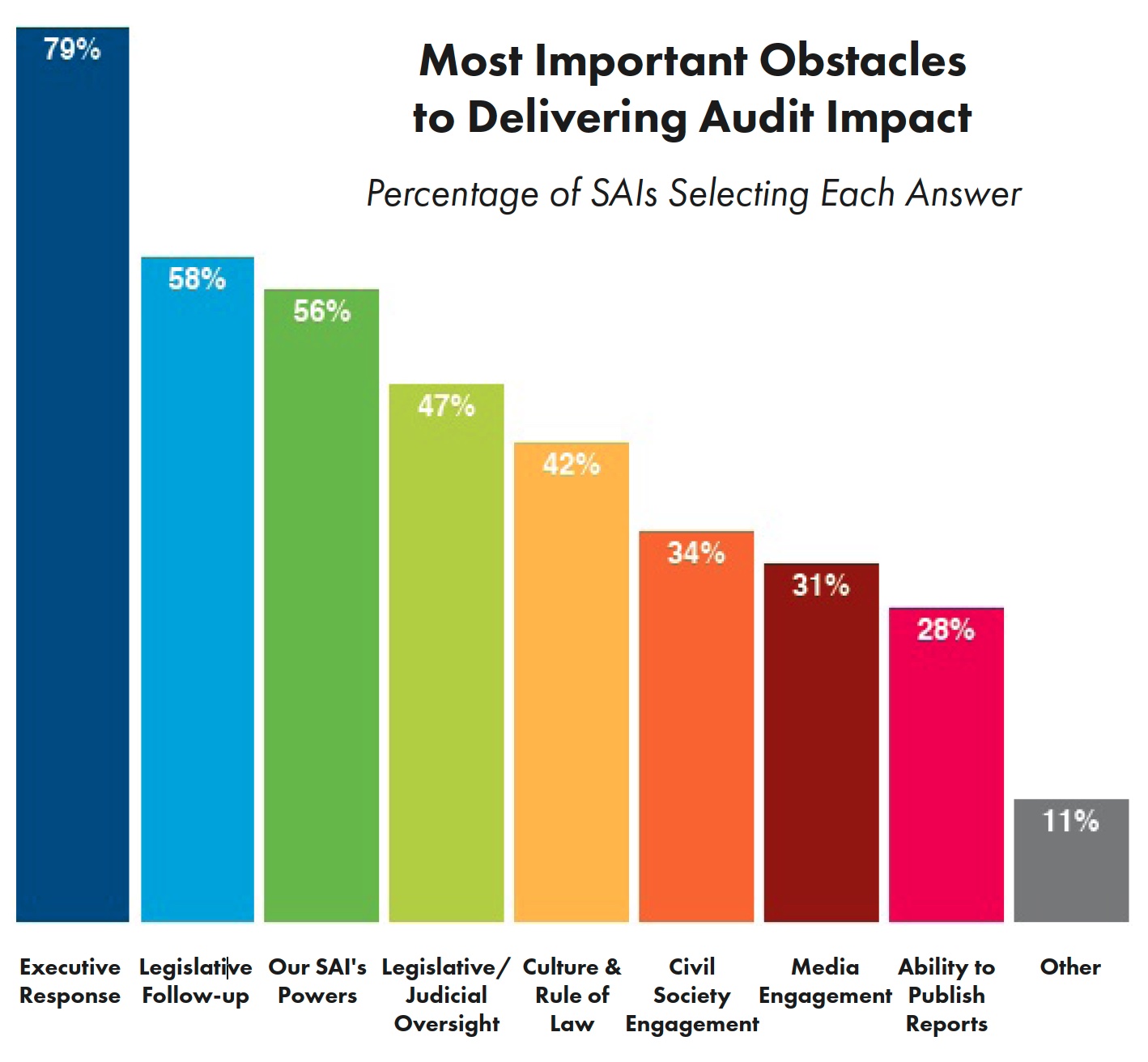

A key indicator for the impact of SAIs is the extent to which audited entities implement their recommendations. SAIs reported that from 2017 to 2019, only half of their recommendations were implemented. The Global Stocktaking shows a sharp drop in the percentage of SAIs that had an internal system for following up on recommendations, which could have contributed to lower audit impact.

SAIs reported that a lack of response from the executive and of follow-up from the legislature were the greatest obstacles to achieving audit impact, a finding supported by Open Budget Index data. However, fewer than half of SAIs said they involved the executive and legislature when following up on the implementation of audit recommendations. Many SAIs communicated regularly with these stakeholders, but their manner of doing so was not always strategic.

While SAIs should be mindful of alliances that could affect the perception of their objectivity, they could make greater use of executive and legislative stakeholders to help governments better understand how to use audit findings. Moreover, some issues are more systemic in nature and therefore need to be communicated at a higher level than solely to the entities under scrutiny. The survey’s findings reaffirm the importance of approaching audits holistically and focusing on strategic communication with key stakeholders.

INTOSAI Bodies and SAIs Provide Crucial Support

The report confirms the important role of INTOSAI regional bodies as frontline providers of guidance, tools, and support to SAIs. Survey results suggest that these organizations— with their unique understanding of regional context—were responsive to SAI needs and developed their initiatives with members' input. They most strongly supported audit capacity, but have the potential to do more to help SAIs enhance other areas as well. In addition, the Global Survey found widespread use of the standards, guidance, and resources developed by other INTOSAI bodies, such as the Goal Committees.

The Global Survey also provided an opportunity to assess how INTOSAI members work with one another. Cooperative audits continued to be a popular means of collaborating and sharing knowledge, with 75 percent of respondents, from all regions, having participated in these efforts.

Seventy-one SAIs reported they had provided peer-to-peer support to other SAIs, down from 87 in 2017; this drop may be due to the reported need for external financing for these efforts. While 67 SAIs said they were willing to lead or support these initiatives in the coming period, the demand for peer-to-peer support cannot be met without additional donor partners.

| |

To read more, click here. |